Development Goals has led to evolution and acceptance of ESG framework that intents describe areas needing specific attention and importance to build a better and a sustainable world. The UN Global Compact and their ever-increasing regional associations have set forth to achieve a better and more sustainable future for all by 2030. These goals target to explicitly on challenges like poverty, health and education, in order to reduce inequality, and infuse economic growth with ownership and responsibility for other critical issues like climate change and scarcity of resources.

The Industries, Markets and customers are tuned on to take the initiatives and responsibility to integrate ESG in all aspects of business and life across markets and countries. The UN’s Principles for Responsible Investment is an international organization that drives initiatives to promote the incorporation of environmental, social, and corporate governance factors (ESG factors) into investment decision making, and encouraging not only investors but stakeholders to take greater responsibility with their investments.

PRI encourages and promotes to adapt to policies related to disclosures as indicated by the proposed renaming of the existing Business Responsibility Report (BRR) to the Business Responsibility and Sustainability Report (BRSR) and encouraging investors to use responsible investing in order to better manage risk and enhance returns on their investments.’ The principles of responsible investment (PRI) have set forth the six basic principles to guide investors while they incorporate environmental, social, and governance (ESG) factors in their investment analysis and decision-making. These principles are as described below:

- Incorporate ESG issues into investment analysis and decision-making processes.

- Become active owners and incorporate ESG issues into ownership policies and practices.

- Seek appropriate disclosure on ESG issues by the entities in which one would invest.

- Promote acceptance and implementation of the principles within the investment industry.

- Work together to enhance effectiveness in implementing the principles.

- Report activities and progress towards implementing the principles.

These principles precisely lay the foundation to promote responsible and stainable business practices that would ensure reduced risk, generating long-term value and while contributing towards building a more sustainable global economy. It has been quite a while that people started taking the responsibility to take initiatives to develop a sustainable economic system for all important aspects of human life pertaining to economic, social and governance connected directly or indirectly.

There have been stages starting in the early 1960s to 1990s where the initial idea took the conception due to evolution of categories of companies producing or providing socially detrimental products and services. The second phase lead to the period of Integration of responsibility during 2000’s where weightage has been given to attach and integrate responsibility to investment decision making.

A lot has started catching attention during the third phase of engagement during 2010’s to see initiatives to engage companies, agencies in adopting sustainable practices to influence and impact the markets. The current and critical stage post 2020 is estimating and assessing the impact to find out evidently the positive and negative material outcomes and developing a long-term approach towards the changes introduced and further required.

In India ESG is driven more from the perspective of market and regulation but the developments in merit greater analysis as India accounts for its population for approximately more than 1.4 billion and still increasing. It is not only the most populous countries in the world but it also attracts significant domestic and foreign investment across varying asset class and numbers are still increasing for Indian companies that compete in the global product (and services) and capital markets.

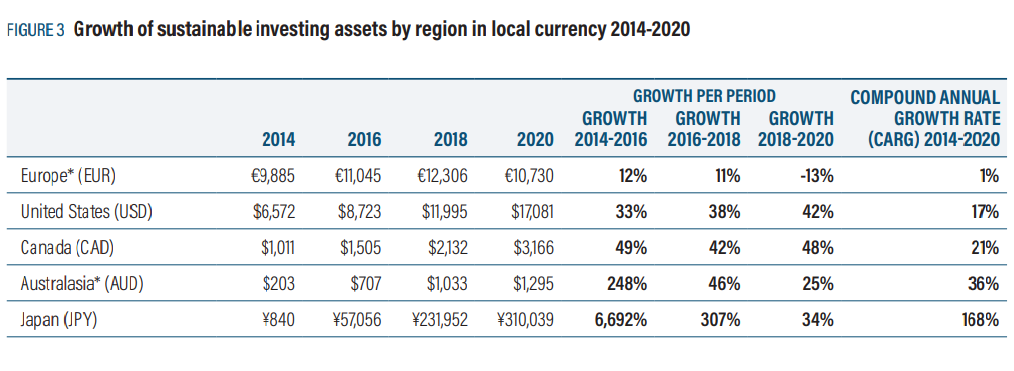

As given in the table above, The GSIR Report of year 2020 presented the data of increasing proportion of sustainable investing across Europe, US, Canada, Australia, and Japan. The compound annual growth rate that these countries have reported is consistently increasing year by year with highest growth being registered by Australia and Japan and with 36% and 168% in their local currency.

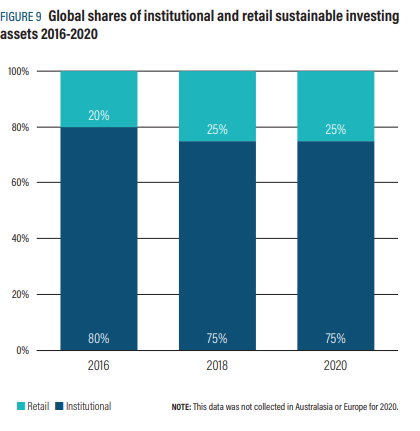

The institutional investors although are the largest dominating participant in the financial markets, the reports have clearly registered the increase in the interest of retail investors in sustainable investing during 2016 to 2018. The reports have seen a steady steadily growth in rising interest of retail investors since year 2012 where the retail investment was just 11% in contrast to institutional investors holding 89% of assets.

*The justification of stable retail position during 2019 1nd 2020 cannot be ignored with the fact that the years were crucial years and have caused a huge impact due to Pandemic across the global countries. The markets however have demonstrated power packed resilience and continued its participation graph.

A recent study by Sharma, P., et al. 2020 conducted the study to examine the extent of environmental, social and corporate governance (ESG) disclosure of Indian companies and verify the relationship between financial performances with ESG framework and compliance. It is proved in the study that factors of profitability measure taken in the study i.e.

ROA and ROCE of a company are positively correlated with ESG disclosures. These results are in line with the earlier results derived in similar studies (Lapinskiene and Tvaronaviciene 2012; Siew et al. 2013b; Ghosh 2013; Breuer and Nau 2014; Tarmuji et al. 2016). However, the findings are limited to the context of thestudy, and study was restricted to Indian companies listed at Bombay Stock Exchange between 2013–2016.

There are studies that emphasise to account more focus on directors’ duties to consider shareholders as well as other constituencies to lay a strong statutory foundation for the legal recognition of ESG, both on a financial basis and an entity approach.

This ESG integrated statutory foundation should be coupled with strong ESG reporting and regulatory framework by the Indian financial regulators (including SEBI) to encapsulate ESG concerns as part of shareholder stewardship initiatives.

The regulators although have significantly tied on the measures towards ESG in India, several challenges however remain, and the efforts thus far can only be work-in-progress. The most critical criterias and sub-criteria amongst environmental, social and governance factors that may impact individual equity investors’ investment decisions have been investigated in a study that was conducted using the MCDM technique, i.e. Fuzzy AHP. using global weights that came out stating’ Governance’ to be the most influential criteria. The other two; environmental criteria are relatively less important whereas social is the least amongst all three.

The corporate governance provides a strong base by laying rules to regulate the corporate functioning, keeping interests of all stakeholders aligned. Since the study specifically targeted individual investors from a specific region hence the findings may not appropriately find fitting well on institutional investors and investors across other regions differing on demography and other dynamic factors.

The increasing importance of principles of responsible investments, there is a considerable demand for esg integration and reporting for non-financial data. It is evidently seen with companies that have obtained got them assessed by esg rating agencies display altogether different performance pictures. The outcomes of the study statestwo important challenges; the availability of the scores and the divergence among them.

The literature on integrated esg reporting clearly explains that ESG information is especially critical in emerging economies in order to reduce agency issues and improve corporate governance. Unavailability of requisite data and lack of evidence about ESG disclosure in evolving financial markets provide a feasible environment to test and study the implications of heterogeneity and ownership structure of boards and its strategic corporate decisions.

There are studies that enlightens the scope of responsibility aligned to leaders differently at different levels where business leaders worldwide make use of all information’s pertaining esg risks and opportunities to use it effectively to engage with investors and other stakeholders. On the contrary, the leaders at global, national, and international levels see itas and moral ethical responsibility to adhere and adopt practices that ensures sustainable future to communities across the globe. It is therefore more of need analysis aligned to carefully selected goals that drives effective engagement with investors and other stakeholders.

There are studies that focused on improving ESG reporting regulations, to improve quantity, quality and corporate ESG performance. The findings urge on the need to provide data that is timely, relevant, credible, and comparable and is therefore capable of demonstrating improved ESG performance. There is a scope to explore on changing consumer preferences and how these preferences may drive improvements in ESG performance.

The broader description in the study on ESG disclosure highlights on quality and comparability of information. In a similar study Cardoni et al., [5] noted that the comparability issues in ESG disclosure is a matter of concern and needs urgent attention.

ESG data serves the diverse interests of investors; a coherent framework for sustainable investing requires methodological construct of standards for collection, aggregation, validation of ESG data; Materiality-based standards identifying factors that drives to explore financial risk and compile opportunity; Metric standards that are well demonstrated in a trusted and carefully structured way for all social and environmental benefits delivered by companies. It is confirmed in a study that financial materiality has a impact in the value of ESG scores and rankings, that helps identify investment opportunities across basis high scores of critical ESG issues.

The study through its study on European stock- listed companies contributes a strong finding that companies mostly (approx. 72%) are not opting external ESG rating, which excludes and limits the approach and authenticity of asset managers who shall rely on the third-party sustainability evaluation for their investment policies. The data studied clearly demonstrates that the sample under study has a higher concentration of high-scoring companies than the findings by Lopez & Bendix (2020) from a global sample.

Methodology: The study applied literature review for exploring the current trends and drivers in integration of ESG framework in Investment decisions and analysing the key barriers including reliability, correctness, completeness, consistency, and integrity of the available information (Jonsdottir, B., Sigurjonsson, T. O., Johannsdottir, L., & Wendt, S. (2022). Barriers to using ESG data for investment decisions. Sustainability, 14(9), 5157) .

The systematic literature review has been done using Scopus indexed papers, journals and high-quality articles published at various national and international online platforms. The Search is carried out on the Google Scholar database on the topic “ESG Framework in investing with combinations of “Key drivers and Barriers in ESG Integration in Investment,” “ESG trends in stock market”, and “Sustainable Investing and Finance”. The studies covering the selectively searched keywords only have been selected for the purpose of further analysis.

After reading the selected research papers and articles, the main factors identified through the study of these papers were identified detailed analysis of each of these factors has been done. The factors at various ends are categorised into geographical, investor profile, asset class of investment to connect and study in detail the limitations and challenges practically posed in integrating ESG framework in investment analysis of any stock or a company chosen for investment.

- Drivers which will include Table 1 and its explanation

The benefits of integrating ESG in investing instigate an approach to “promote investment with a long-term time horizon” and the other following by “improving the better investment practices.” Integrating ESG in investment is driven more by markets, as majority of beneficiaries demand inclusion of ESG. The investors and asset managers however also have a similar opinion that their interest is driven more by mandatory regulatory requirements and peer pressure across their choice of investments.

A substantial portion of asset owners and managers seems to carry considerable confidence that choosing “ESG aligned long-term asset selection and its performance” is comparatively better than the ones who ignore its relevance during their decision-making process. However, this motivation of Asset owners vary from country to country as asset owners in Asia Pacific are claimed to be more motivated by the integration in comparison to America, Europe, Middle East, and Africa.

Table 1. Drivers in ESG integration into Investment Decisions

| Industry Drivers | Transparency and Uniformity Building Investment Models Availability of Big data Managing investment risks Identify investment opportunities Contributes to financial performance Brings Reputational benefit |

| Market Drivers | Demand from Beneficiaries Outperformance by funds Fosters long-term investment mindset Long-term Incentives |

| Governance Drivers | Creating Institutional legitimacy. Ascertaining fiduciary duty of trusts. Proxy for management and leadership quality. Regulatory requirement of performance reporting. |

spite of huge structural and policy evolution on ESG to aim sustainable investing and finance, it is uncommon for investors to carry perceived barriers and pre conceived conclusions of witnessing underperformance. It is claimed that ESG based investing requires compromising on immediate returns and it violates the fiduciary duty of investing managers aiming to maximise returns, which is detrimental to investors’ short time frames for outperformance.

The perceived approach that funds fiduciaries should ideally not take ESG framework into account because of their primary responsibility of maximizing the returns to their beneficiaries is challenged by various studies and reports.

There is a very small segment of investors that view regulations or the general counsel’s interpretation of fiduciary duty to act as a barrier to integration of ESG in planning Investment and decision-making criteria and the larger portion of asset owners and managers still agreeing that the focus of fiduciary duty is shifting toward promoting integration of ESG framework without detrimenting the fair competitive returns on investments.9

(9. Eccles, Robert G., Verheyden, Tim & Feiner, Andreas. “ESG for All? The Impact of ESG Screening on Return, Risk and Diversification.” Journal of Applied Corporate Finance, Volume 28, no.2 (2016). Pages 47-55.

Link:https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2834790.)* (Clark, Gordon, Feiner, Andreas & Views, Michael. “From the Stockholder to the Stakeholder: How Sustainability Can Drive Financial Outperformance.” Arabesque Asset Management and Oxford University (2015).

Link: http://www.arabesque.com/index.php?tt_ e2de00a30f-88872897824d3e211b11)

The Principles for Responsible Investment (PRI) also in its several studies11 (See Justin Sloggett, Don Gerritsen, and Mike Tyrrell; “A Practical Guide to ESG Integration for Equity Investing.” Principles for Responsible Investment, United Nations Global Compact, United Nations Environment Programme Finance Initiative (2016).

Link: https://www.unpri.org/news/pri-launches-esg-integration-guide-for-equity-investors. ) has suggested it would in fact be viewed as a failure of fiduciary duty not to take ESG criteria into account.12 (12. Alice Garton, “New QC Legal Opinion Confirms Pension Fund Trustees’ Legal Duty to Assess Climate Risk.” Client Earth Investor Briefing (2016).

Link: https://www.documents.clientearth.org/wp-content/uploads/library/2016-12-02-investor-briefing-new-qc-opinion-pension-trustees-and-climate-risk-ce-en1.pdf. ).

The changing economic, social and market dynamics has caught a huge attention on sustainable and responsible investments and urges the need to integrate ESG factors significantly to ensure sustainability. It is an emerging evolution and the need of the hour to research actively on ways to ensure development and sustainability hand in hand.

The Private Equity (hereafter stated as PE) firms are actively integrating these factors into their investing strategies and research activities. There are results from several studies that shows most PE firms integrate ESG aspects because of increasing conscience on these trending issues from the perspective of an investor and the stakeholders.

CFA Institute (CFA 2017) through its research has also confirmed that institutional investors are generally considering ESG issues systematically in their investment analysis, and there is similar result obtained in the study (Amel-Zadeh and Serafeim 2017). There is consistent growth in understanding that ESG factors have a material impact on the overall corporate performance and on financial market as a whole.

Several researches suggest that financial markets reward good ESG practice, while a low score on ESG scan leads to a gradual drop in the overall market value of firms (especially in case of spread of negative information) or increasing required rate of return to compensate for risk premium (Bauer and Hann 2010; Credit Suisse 2015).

The findings of the study also revealed that the basis of integration was also supported by clients demand and management quality and amongst the other key reasons, investors stayed focused on emphasizing importance of ESG in managing investment risk and its analysis.

The study also brought clarity on ESG factors truly not integrated in fundamental analysis and the integration mostly being discretionary and unsystematic in nature. There are some material reasons explained in the report (Eccles & Kastrapeli 2015) that the greatest barrier in the integration of ESG is the lack of standards for measuring and comparing ESG performance due to lack of availability of ESG performance data that should ideally be reported by companies as mandatory disclosure.

Similar results were found in a survey (Amel‐Zadeh and Serafeim, 2015) where the key issue in integrating ESG found is lack of comparability across firms, missing data usefulness, lack of quantifiability, followed by missing reporting standards and increasing cost.

The findings also disclosed another strong obstacle that attracts concern is perceived fear of underperformance and increasing cost which is also confirmed in a study of (CFA 2017). The study through its findings emphasises that there is a lack of appropriate quantitative ESG information, lack of comparability and questionable data quality across firms.

2. The markets though are witnessing various external forces pushing the PE industry towards tshe ESG integration. It has also emerged that integration of ESG factors leads the way to efficiently manage risks and create value for the investors. However, during the various studies conducted, it has also been found that there are several barriers in integrating the ESG framework in investment decisions, the most critical amongst it is indigenously used in-house tools to assess ESG factors and there are only few firms that use external advice from industry experts.

These PE firms face, the critical issues like finding accurate, reliable, and comparable information along with the lack of comprehensive ways to measure these types of issues.There are several studies that have lead to identification of few critical barriers to its integration as given below;

| Industry Barriers | Lack of performance measuring standards. Lack of Corporate ESG Performance reporting (Accuracy, reliability, and comparability). Fear of concluding underperformance. Time consuming and costly. |

| Market Barriers | Lack of external advisors with relevant experience. Lack of in-house professional skills. Lack of training and guidance. Personal biases and beliefs of Senior leaderships. |

| Governance Barriers | Lack of dialogue and distinction of Fiduciary responsibility. Regulations on or general counsel’s interpretation. Lack of concern about integrating standard approach. |

3. There are growing number of corporations that are now using standards issued by Global Reporting Initiative to evaluate and report their initiatives and efforts under economic, environmental, and social impacts [47](Brown, H.S.; De Jong, M.; Lessidrenska, T.

The rise of the Global Reporting Initiative: A case of institutional entrepreneurship. Environ. Politics 2009, 18, 182–200. [CrossRef]). It clearly emerged in various reports that this emphasis on ESG factors is a way to manage risks since there are fewer PE firms that carry an approach to review companies’ environmental and social issues to count and create value.

In line with these results, we found that the tools mainly used to assess ESG factors are broadly the checklists and that there are very few firms that use external advice from industry experts. We contend that checklists are a useful tool for PE firms willing to perform a company’s ESG assessment in order to reduce risk, but external advice from industry experts should be complemented if the PE firm wants to open market opportunities and spur innovation. With regard to the findings, It can be said conclusively that the main barriers that firms face are difficulties in finding relevant information and the lack of a comprehensive ways to measure similar issues.

4. It seems justified to rest assure on reasonable justification that one of the root cause on account of the mentioned information and its issues is the existence of variety of guidelines to define standards for ESG reporting, the best knowns are: the GRI4 (Global Reporting Initiative) standards, the Integrating Reporting5 (IR) standards, and the SASB6 (Sustainability Accounting Standards Board) standards that regulate and develop sustainability accounting standards for 79 industries in 11 sectors.

Apart from this, there are some other international and national corporate reporting standards too, including ISO 26000 2010 Guidance on social responsibility7, Management Discussion and Analysis national guidelines, National standards of Sustainable Development Reporting, for example Guidance Documents by RSPP (Russia) that make the entire system clumsy and entangled.

I Business Institute, Greater Noida

Business Institutes in Delhi-NCR

Website: www.ibusinessinstitute.org

Email: [email protected]

Helpline No: +91-7065333326/27